Despite the latest positive signs, no one really knows where the US-China trade war is heading, but neither the global nor China’s economy is suffering as much as feared.

China’s economy currently surprises more positively than negatively, which was probably not the intuitive expectation when considering the consequences of the trade war. I find it very encouraging that the corporations’ own expectations (PMI index) based on the latest release from Monday, 2nd September, showed a move back in the positive territory. For the manufacturing sector, the index rose to 50.4, which is in the expanding territory, and for the service sector, the index is now at 52.1, after a dive down to 51.6 last month.

However, the pressure from the trade war is of course apparent, like one can observe in graphic one, showing the annual change in China’s industrial production. Despite that annual growth is higher than in many other countries, the growth rate last month was somewhat below expectations.

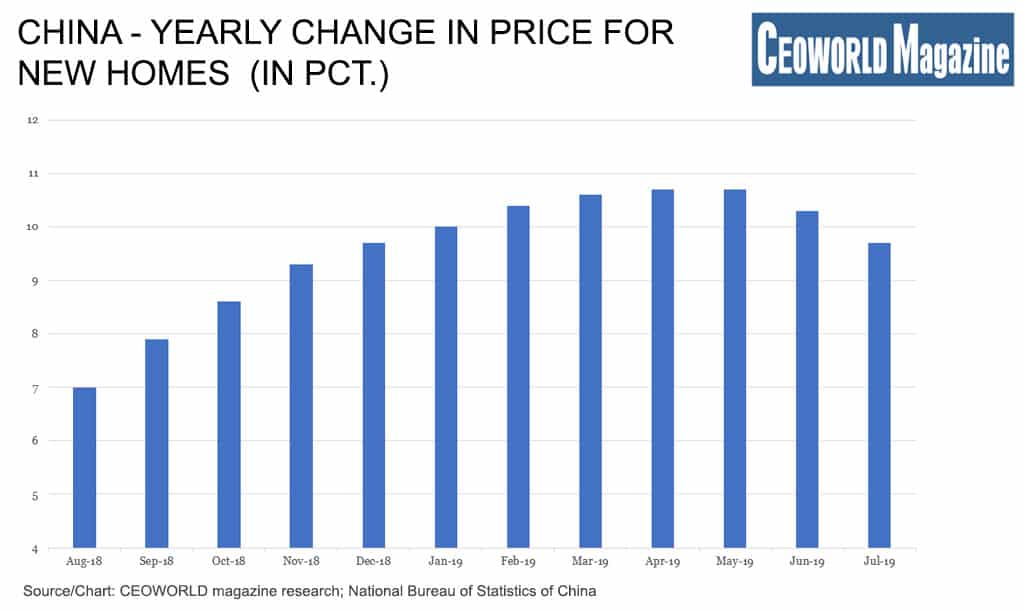

However, the negative development in the industrial sector does not spread significantly in China’s economy. As graphic two shows, even the annual rise in house prices continues to remain on the high end, despite official efforts to cool the market. The real estate market will cool down further, but nowhere is a crash in sight.

I find the latest batch of economic data from China interesting, because they once again set the fear about the country’s economy in perspective. There is no doubt that the US trade war is hurting China’s exports, and for example the industrial sector. However, the general global headwind that blows across the world should be deducted when one determines the real effect of the trade war.

I am well-aware that the global economy is shifting gear partly due to the trade war, and thus, it all has a self-reinforcing effect.

This constellation of factors affecting the economy reminds me a bit about the “chicken or egg” discussion. It is therefore a kind of noise when giving an assessment of China’s economic situation. Because how much of the headwind is due to the trade war, and how much is simply related to the general decline in the world economy?

Of course, there is a correlation between graphic one and the US trade war against China. When correcting for the general downturn in the global economy, it is my assessment that Trump’s trade war has had a noticeable effect on China’s economy, but no more than that- which is until now, not a catastrophe for China.

If one looks at how many and how strong forces at present are destructing economic growth, then global GDP growth would long have been negative, if the world economy had lacked robustness.

The worst forces that weigt on the global economy are, of course, the US-Chinese trade war, a Brexit where no one understands the dispute anymore, and a European continent that is in a complete standstill and incapable of action.

It should have sent global economic growth in a deep dive, but so far, it has resulted in a headwind, though not a crash as one would fear. Based on this sort of negative test, I argue that the global economy is actually doing reasonably well.

However, more of the current political “masterwork” can naturally derail the global economy completely, including China’s economy. But right now, my position is that the robustness is winning, and my assessment is that as a consequence of this “positive” view, too much fear is priced in the financial markets.

I actually perceive China’s economy as particularly robust. This is a contrariwise position compared to the eternal nervousness that surrounds China’s economy in the financial markets and among economists.

In my view, an important argument for being less concerned about China’s economy than most investors are right now, is the macroeconomic figures that I initially described. Here, I argue that they mainly represent the function of the general slowdown in the global economy, rather than a downturn due to the US trade war.

Further, I find it very interesting that the Chinese government and authorities apparently still consider the economy so robust, that they continue to close or relocate factories that pollute too much.

Though it should be mentioned that a development like in graphic one has reduced the authorities’ appetite for the green transition by closing factories.

One of the reasons why China’s economy so far has absorbed the pressure from the trade war without a deeper dive is due to the fiscal countermeasures implemented by the government. The actions range from tax cuts via public investment to a variety of subsidies to different sectors.

My best bet is that the government will introduce another round of similar fiscal stimulus again before the year is over.

Combined with the basic robustness, which I claim that China’s economy has, I do not expect growth in China to surprise negatively this year, nor into next year. If President Trump continues his trade war, especially against China, then I think it’s more likely that he forces the US economy into a downturn.

The same thoughts are probably also being considered in Beijing, and therefore my expectation is that any fiscal measures will support two significant goals. The first is to move the Chinese domestic economy increasingly and swiftly, towards becoming its own single market- that movement has long been under way, but is now intensifying.

The next element is to prepare China’s economy and growth for a trade war that could last until President Trump’s tenure possibly ends after the next US presidential election.

My assessment is not that it is China’s preferred goal to prolong the trade war, and it remains my primary scenario that US and China will enter some kind of agreement in December or January. Should this not be the case, then I argue that China’s economy will suffer less than the financial markets fear, even if the trade war drags out.

Graphic one: China- Yearly change in industrial production (in pct.)

- Aug-18: 6.1%

- Sep-18: 5.8%

- Oct-18: 5.9%

- Nov-18: 5.4%

- Dec-18: 5.7%

- Jan-19: 5.3%

- Feb-19: 5.3%

- Mar-19: 8.5%

- Apr-19: 5.4%

- May-19: 5%

- Jun-19: 6.3%

- Jul-19: 4.8%

Graphic two: China- Yearly change in price for new homes (in pct.)

- Aug-18: 7%

- Sep-18: 7.9%

- Oct-18: 8.6%

- Nov-18: 9.3%

- Dec-18: 9.7%

- Jan-19: 10%

- Feb-19: 10.4%

- Mar-19: 10.6%

- Apr-19: 10.7%

- May-19: 10.7%

- Jun-19: 10.3%

- Jul-19: 9.7%

Written by Peter Lundgreen.

Have you read?

The World’s Safest Cities Ranking, 2019.

The Best Hotels In New Delhi For Business Travelers, 2019.

Best CEOs In The World 2019: Most Influential Chief Executives.

Countries With The Best Quality of Life, 2019.

World’s Best Countries To Invest In Or Do Business For 2019.

Add CEOWORLD magazine to your Google News feed.

Follow CEOWORLD magazine headlines on: Google News, LinkedIn, Twitter, and Facebook.

Copyright 2024 The CEOWORLD magazine. All rights reserved. This material (and any extract from it) must not be copied, redistributed or placed on any website, without CEOWORLD magazine' prior written consent. For media queries, please contact: info@ceoworld.biz