The Profit Formula® is just one of 8 Scientific Perfections Business Economics

From the outset, SVD does not exist fiscally, and the same applies to both IFRS and US-GAAP until the present day. So, from the beginning, SVD has to be set simply equal to zero immediately. Regarding fiscal accounts and the accounts to be published e.g. IFRS and US-GAAP (financial accounting, ‘de jure’) then only NVD has to be mastered presently.

The filling in of the value of any asset at the start and end of the period under consideration results in one NVD-figure. The value at start is the value at the end of the previous period. One has to fill in only the new end values i.e. the required fiscal values respectively IFRS or US-GAAP values according the concerning closing balance sheet.

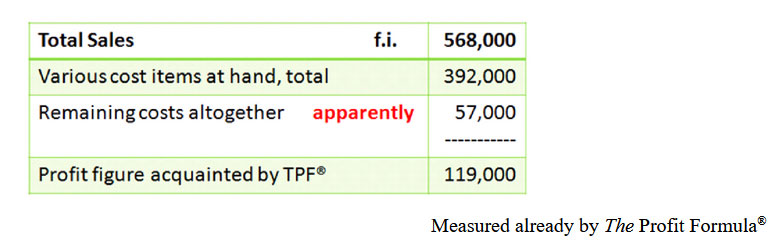

Fiscally and for both IFRS and US-GAAP, certain cost items are prescribed in the required reports. The fiscal profit figure as well as the profit figure to be published can be calculated easily by means of The Profit Formula®, which ignores costs. Subsequently, various cost items – because the required reports naturally need to be complete – can still be determined, in fact now more easily since the figure on the bottom line is already available.

Firstly all cost items which are at hand aggregated and secondly the already known profit figure that is measured by The Profit Formula®, ending up in one item in between i.e. ‘remaining costs all together’ that simply is falling from the sky.

The same applies for fiscal as well as published profit figures (f.i. IFRS or US-GAAP).

The charm of The Profit Formula® is its simplicity. Other systems for determining profit use all kinds of detours to reach the same result at the most, depending on the set of values and standards which was used. The Profit Formula® works at both any value and any standard.

The profit is an ‘after the fact’ figure. When it concerns an entire year, we look back on the annual profit figure, as it were, with our backs to the future. While the company might well be heading straight for a disaster. Thus considered, profit figures are of little use. Profit, however, is not only the consolidated annual profit of a group, but it mainly consists of the detail profits of one specific activity or company unit for short periods.

Knowledge of these profits is essential to give guidance and to be able to adjust. In the end good management is about creating increased value, it is as simple as that. The total of the profit for a period is the sum of its parts. The profit on each product in that period is a part. The profit in addition to its composition, the profit contribution of each product (or part of the range), of each customer (or district or market segment), who would not want to be well informed on these matters?

One can compare a company with a gang of skaters in a tournament. Some of them choose longer and others shorter distances. Different products, activities, units, divisions. The total result of the gang in the tournament is the addition sum of individual achievements. A year-ride, 13 rounds of 4 weeks each. Lap times. From lap to lap, how many fingers of the coach go up, down?

Acceleration and slowing-down during a race can be calculated by measuring the lap times. Without knowing the lap times, it is difficult to say anything meaningful about accelerations and decelerations during the course of the race. Measuring the lap times, it is for this reason that one is sorely in need of a user-friendly period profit measuring instrument, above all quick and easy to use.

Here, it is: The Profit Formula®

<Profit = (CASH -/- NVD)(1 -/- quota) -/- SVD>

Integration of nominalism (NVD) and substantialism (SVD)

In examples at institutes, Business Schools and Universities, there are just a few transactions. In practice, thousands, if not tens of thousands of transactions and countless interim price changes, will soon be involved. For the profit calculation with one of the current profit determination systems, all transactions must be calculated exactly. What a work. Inefficient. A real waste.

Not necessary when using The Profit Formula®. Count everything together: the total sales minus the total purchases is CASH. Furthermore, it only concerns a few initial and final values (filling in NVD and SVD) and it is ready. The Profit Formula® implicitly takes into account all interim price changes and all transactions. You do not have to worry about it anymore. That saves a lot of work. The counting and calculation work has been reduced to an absolute minimum. For that reason alone The Profit Formula® is second to none. The Profit Formula® works always and everywhere. Effective and efficient.

It takes much effort to get through exercises in the traditional way, sales minus costs, where sustainable means of production are treated differently than units of trade goods. It causes a lot of headaches. The Profit Formula® is still not used by colleges and universities, business schools worldwide. Don’t ignore The Profit Formula®. Students, if they neglect, protest against your trainers! The scientific substantiation of The Profit Formula® is explained in ISBN 9781086333992 Scientific evidence as well as practical application.

Once upon a time, till the late seventies of the twentieth century, inflation accounting was about the search for the one and only real period profit. Economists and accountants could not solve the problem. “The accounting profession proves unable (or unwilling) to deal with the problem of inflation accounting (Tweedie, Whittington, 1984, p. 346-348).”

CEO and CFO, by now, if you still do not know what the real profit is and hence the real yield is also unknown, you cannot know if you are doing the right things, and it’s your own fault not using The Profit Formula®.

CEO and CFO, by now, if you still do not know what the real profit is and hence the real yield is also unknown, you cannot know if you are doing the right things, and it’s your own fault not using The Profit Formula®.

The Profit Formula® is just one of 8 Scientific Perfections described in Business Economics VI Groundbreaking ISBN 9781086355635 (Paperback) and Kindle edition e-book at www.amazon.com

Business Economics VI Groundbreaking ISBN 9789464026405 (Hardcover) at www.boekengilde.nl/boekenshop and www.managementboek.nl

Many outdated study books Business Economics can be replaced by studying this Number 1 from a triptych. Number 2 is a book with exercises; this is the ultimate test for everyone. Finally check everything. Compare your solutions with the complete elaborations in Number 3 from the triptych. Business Economics VI Groundbreaking goes beyond the borders of set science, and rewrites/improves large tracts of business economics as it is currently badly taught worldwide. Suitable for self-study, students, graduates, everybody, even professors can learn a lot from it and each manager will improve performance.

Add CEOWORLD magazine to your Google News feed.

Follow CEOWORLD magazine headlines on: Google News, LinkedIn, Twitter, and Facebook.

This report/news/ranking/statistics has been prepared only for general guidance on matters of interest and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, CEOWORLD magazine does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Copyright 2024 The CEOWORLD magazine. All rights reserved. This material (and any extract from it) must not be copied, redistributed or placed on any website, without CEOWORLD magazine' prior written consent. For media queries, please contact: info@ceoworld.biz

SUBSCRIBE NEWSLETTER